Futures: Overnight, LME copper opened at $8,942.5/mt, fluctuated upward in the early session and touched a high of $9,058/mt near the end of the session. The center of gravity pulled back and touched a low of $8,885/mt at the end of the session, then slightly rebounded and finally closed at $8,977.5/mt, up 0.9%. Trading volume reached 28,000 lots, and open interest reached 298,000 lots. Overnight, the most-traded SHFE copper 2505 contract opened at 74,770 yuan/mt, fluctuated upward in the early session and touched a high of 75,340 yuan/mt during the session. The center of gravity pulled back and touched a low of 74,160 yuan/mt at the end of the session, finally closing at 74,450 yuan/mt, down 0.73%. Trading volume reached 70,000 lots, and open interest reached 145,000 lots.

.

【SMM Copper Morning Meeting Summary】News: (1) On April 9 (Wednesday), Julia Torreblanca, head of the National Society of Mining, Petroleum and Energy of Peru (SNMPE), stated that Peru's copper production is expected to grow by 2-4% this year. This will bring Peru's copper production to 2.79-2.85 million mt, higher than last year's 2.74 million mt.

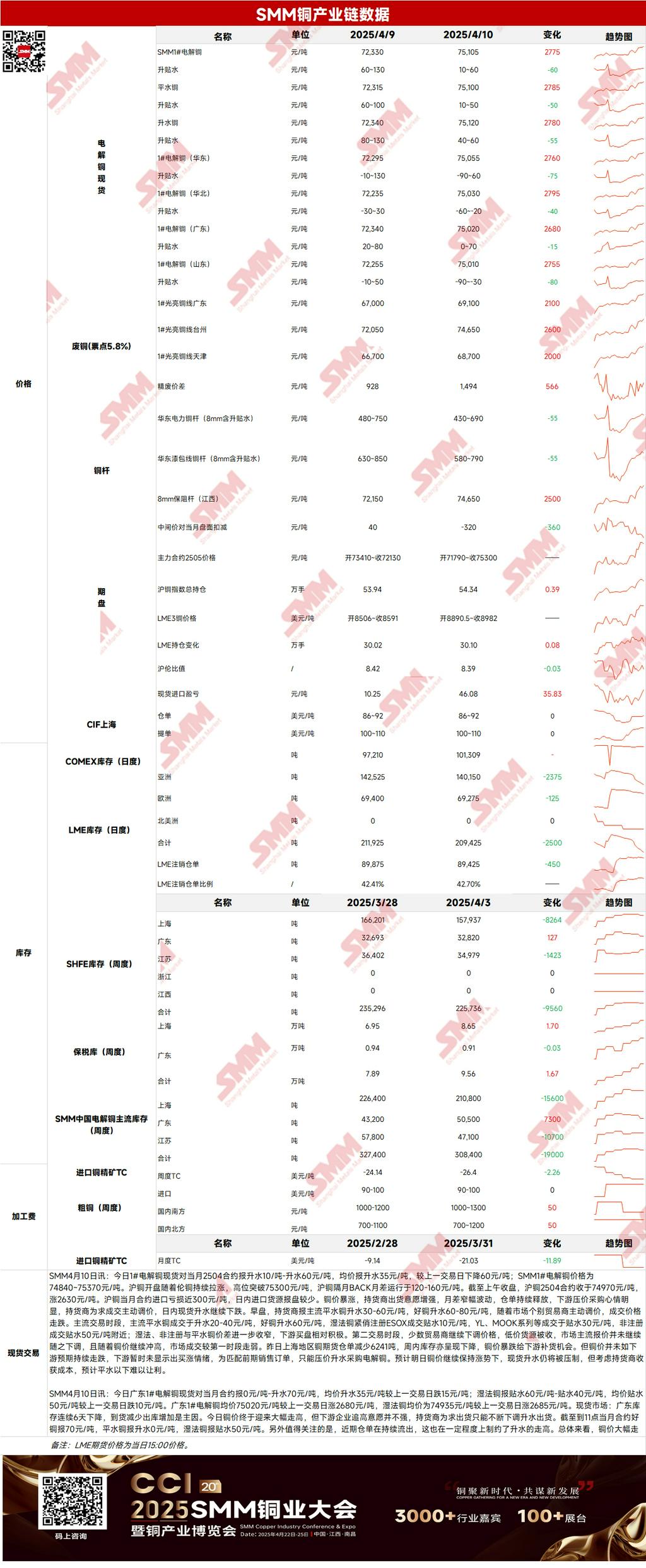

Spot: (1) Shanghai: On April 10, spot prices of #1 copper cathode against the front-month 2504 contract were at a premium of 10-60 yuan/mt, with an average premium of 35 yuan/mt, down 60 yuan/mt from the previous trading day. SMM #1 copper cathode prices were at 74,840-75,370 yuan/mt. SHFE copper opened with LME copper continuing to rise, breaking through 75,300 yuan/mt at the high. The price spread between SHFE copper front-month and next-month contracts ran at 120-160 yuan/mt. As of the morning close, the SHFE copper 2504 contract closed at 74,970 yuan/mt, up 2,630 yuan/mt. The import loss of the SHFE copper front-month contract was nearly 300 yuan/mt, and there were few offers for imported cargoes during the day.

(2) Guangdong: On April 10, spot prices of Guangdong #1 copper cathode against the front-month contract were at 0-70 yuan/mt, with an average premium of 35 yuan/mt, down 15 yuan/mt from the previous trading day. SX-EW copper was at a discount of 60-40 yuan/mt, with an average discount of 50 yuan/mt, down 10 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 75,020 yuan/mt, up 2,680 yuan/mt from the previous trading day. The average price of SX-EW copper was 74,935 yuan/mt, up 2,685 yuan/mt from the previous trading day. Overall, copper prices surged significantly, but downstream buyers were reluctant to chase the rally, resulting in poor spot transactions.

(3) Imported copper: On April 10, warrant prices were at $86-92/mt, QP April, with the average price flat from the previous trading day. B/L prices were at $100-110/mt, QP May, with the average price flat from the previous trading day. EQ copper (CIF B/L) was at $55-65/mt, QP May, with the average price up $5/mt from the previous trading day. Offers referred to cargoes arriving in mid to late April. The SHFE/LME price ratio pulled back in the early session, and warrant offers retreated. Suppliers' willingness to sell weakened, while buyers were very active in inquiring about EQ cargoes arriving in April-May.

(4) Secondary copper: On April 10, secondary copper raw material prices rose by 2,100 yuan/mt MoM. Bare bright copper prices in Guangdong were at 69,000-69,200 yuan/mt, up 2,100 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,494 yuan/mt, up 566 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 880 yuan/mt. According to the SMM survey, secondary copper rod enterprises did not produce during the week due to difficulties in purchasing and limited orders. As copper prices rebounded significantly during the day, downstream ordering sentiment improved. With copper prices continuing to climb in the afternoon, secondary copper rod enterprises had to suspend sales due to insufficient finished product inventories.

(5) Inventory: On April 10, LME copper cathode inventories decreased by 2,500 mt to 209,425 mt. On April 9, SHFE warrant inventories decreased by 7,869 mt to 89,524 mt.

Macro: The US unadjusted CPI YoY in March was 2.4%, hitting a six-month low and below the market expectation of 2.6%. After the data was released, traders bet that the US Fed would resume interest rate cuts in June and could lower the policy rate by a full percentage point by the end of the year, which weighed on the US dollar. The US dollar index once fell by more than 2%, benefiting copper prices. Fundamentals: Copper prices surged today, and suppliers' willingness to sell increased. Warrants continued to be released, and both futures warrants and weekly inventories in Shanghai decreased, indicating some supply release. As of Thursday, April 10, SMM mainstream copper inventories across the country decreased significantly by 31,500 mt from Monday to 267,200 mt, down 46,400 mt from last Thursday, marking the sixth consecutive week of weekly destocking. Demand side, downstream buyers' mentality of driving down purchasing prices was evident. At the same time, as copper prices surged, market transactions weakened, and downstream buyers did not show sentiment of rushing to buy amid continuous price rise, only matching previous orders by driving down purchasing prices. Price side, macro bearish factors weakened, the US dollar weakened, and fundamentals showed inventory declines, indicating that copper prices still have some upward momentum in the short term.